18

for a savings account that calculates interest daily and pays interest monthly, is it better to contribute daily or monthly?

(lemmy.world)

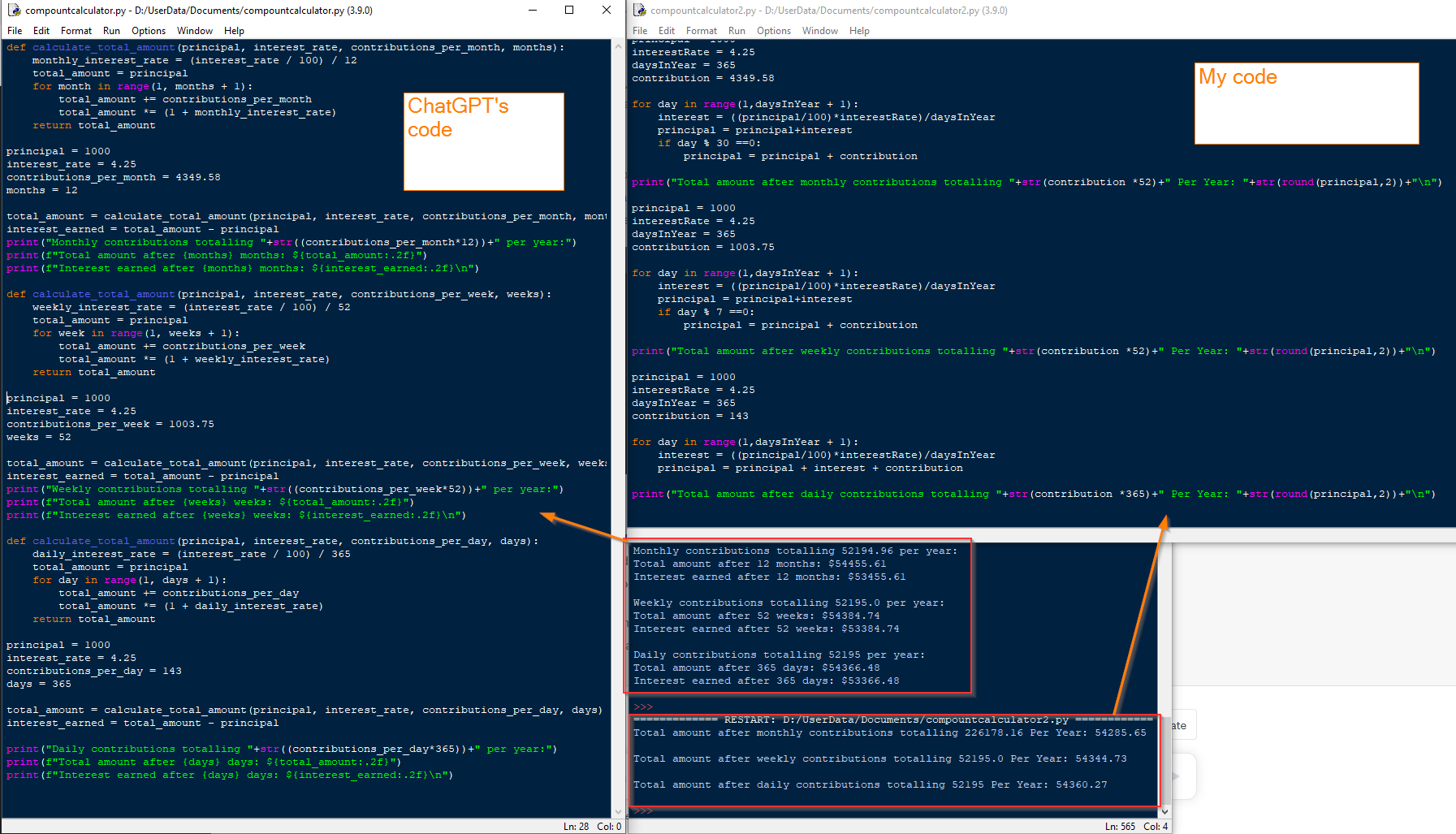

So i got into a disagreement with ChatGPT about whether you earn more interest overall if you contribute daily rather than monthly, if the overall contribution over 1 year is the same.

I made CGPT write some python code to prove it. His code is on the left. I still didnt believe him so I wrote my own, on the right.

Our results seem to disagree, so Im asking you guys, if your interest is calculated daily and paid monthly, is it better to contribute $143 per day for 365 days, or $4349.58 monthly for 12 months?

But I would add, don’t hold back money from your higher interest accruing accounts if you have it, if you’re trying to optimize the interest. Once you have the money, deposit it as soon as possible, so interest begins accruing on it, even if it’s not the beginning of the month yet.

In other words, if you hold back money, it’ll never accrue interest. You’re not going to get exponential or compounding growth on money that wasn’t accruing interest. You only get that once it begins accruing interest.

This is a good clarification. Indeed, ideally you'd want to put your money into that higher-interest vehicle as soon as possible, so basically, the same day you get paid.

In the limit, if you were to receive income once a year, you'd put that into savings immediately, which is maybe on January 1st, or earlier or later, depending on when your actual payday really is.

If you get a windfall, you'd also not want to let it linger on your current account for (next to) nothing, but put it to work as soon as is feasible.

So investing my money into savings right after I get paid weekly is the best strat then, which is what im doing. If i got paid daily, then investing daily would be the best strat.

I wasnt actually trying to minmax my savings interest, I guess I was just confused by the robots' counterintuitive answer but it makes sense now.